Tax Deducted at Source (TDS) continues to be one of the most misunderstood areas of compliance, especially when it comes to rent payments and transactions in goods. With the transition to the Income Tax Act, 2025, many businesses and landlords are struggling to classify payments correctly and avoid penalties.

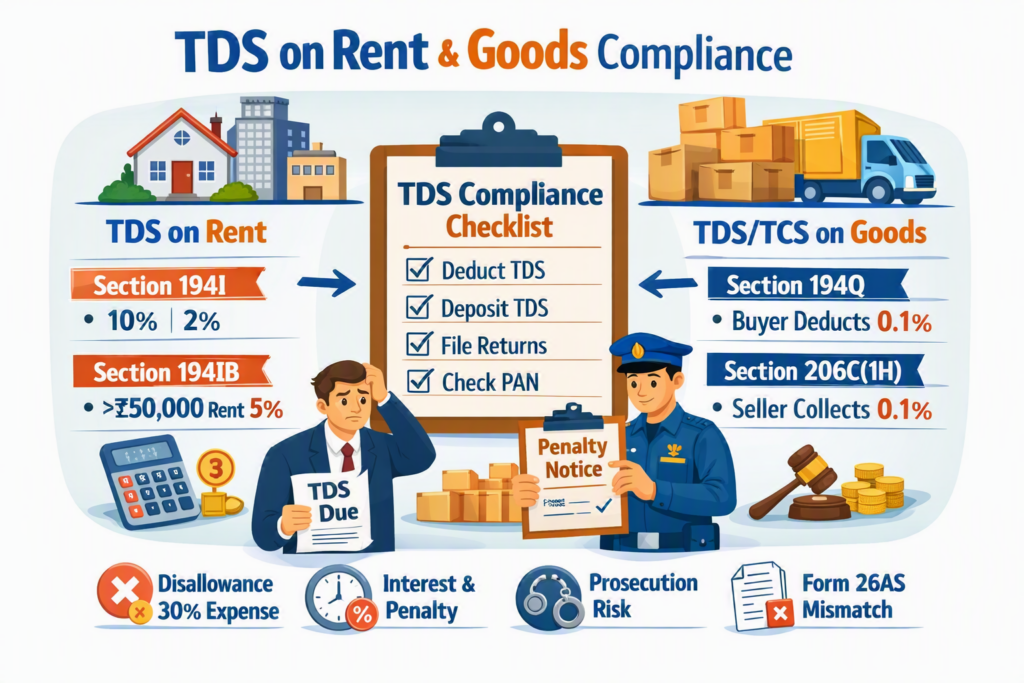

📌 TDS on Rent – Section 194I & 194IB

- Section 194I:

- Applies to rent for land, building, furniture, fittings, machinery, or equipment.

- Rates:

- 2% → Machinery/plant/equipment.

- 10% → Land/building/furniture/fittings.

- Threshold: No TDS if rent ≤ ₹50,000/month.

- Applicability: Companies, firms, and HUFs (if turnover > ₹1 crore business / ₹50 lakh profession).

- Section 194IB:

- Applies when individuals/HUFs (not liable under 194I) pay rent > ₹50,000/month.

- Rate: 5%.

- Deduction only once per year (last month of tenancy).

👉 Common Confusion: Businesses often misclassify rent for machinery under 194I(b) instead of 194I(a), leading to wrong deduction rates.

📌 TDS/TCS on Goods – Section 194Q & 206C(1H)

- Section 194Q (TDS on purchase of goods):

- Buyer with turnover > ₹10 crore must deduct 0.1% TDS if purchases from a seller exceed ₹50 lakh in a year.

- Section 206C(1H) (TCS on sale of goods):

- Seller with turnover > ₹10 crore must collect 0.1% TCS if sales to a buyer exceed ₹50 lakh in a year.

👉 Frequent Confusion:

- Who deducts first – buyer or seller?

- Rule: TDS under 194Q overrides TCS under 206C(1H). If buyer deducts TDS, seller need not collect TCS.

⚠️ Impact on Landlords & Businesses

- Landlords: Must track thresholds and ensure PAN availability to avoid higher deduction (20%).

- Businesses: Need robust accounting systems to classify rent correctly and monitor purchase/sale thresholds.

- Cash Flow: Wrong deductions can block funds until refunds are processed.

- Compliance Risk: Mismatched reporting in Form 26AS can trigger notices.

🚨 Penalties & Consequences of Non-Compliance

Failure to deduct or deposit TDS on rent or goods can lead to serious financial and legal consequences:

- Disallowance of Expense (Section 40(a)(ia)):

- If TDS is not deducted, 30% of the expense (rent or purchase) may be disallowed while computing taxable income.

- Interest (Section 201(1A)):

- 1% per month → for delay in deduction.

- 1.5% per month → for delay in deposit after deduction.

- Penalty (Section 271C):

- Equal to the amount of TDS not deducted/paid.

- Prosecution (Section 276B):

- Rigorous imprisonment from 3 months to 7 years, plus fine, for willful default.

👉 Bottom Line: Non-compliance not only increases tax liability but also risks legal action and reputational damage.

✅ Action Points

- Classify rent correctly – machinery vs building.

- Update accounting software with new section codes (194I(a), 194I(b), 194IB, 194Q, 206C(1H)).

- Monitor thresholds monthly to avoid missed deductions.

- Communicate with counterparties (landlords, vendors, buyers) to align on TDS/TCS responsibilities.

- File returns accurately – ensure deductions reflect in Form 26AS.